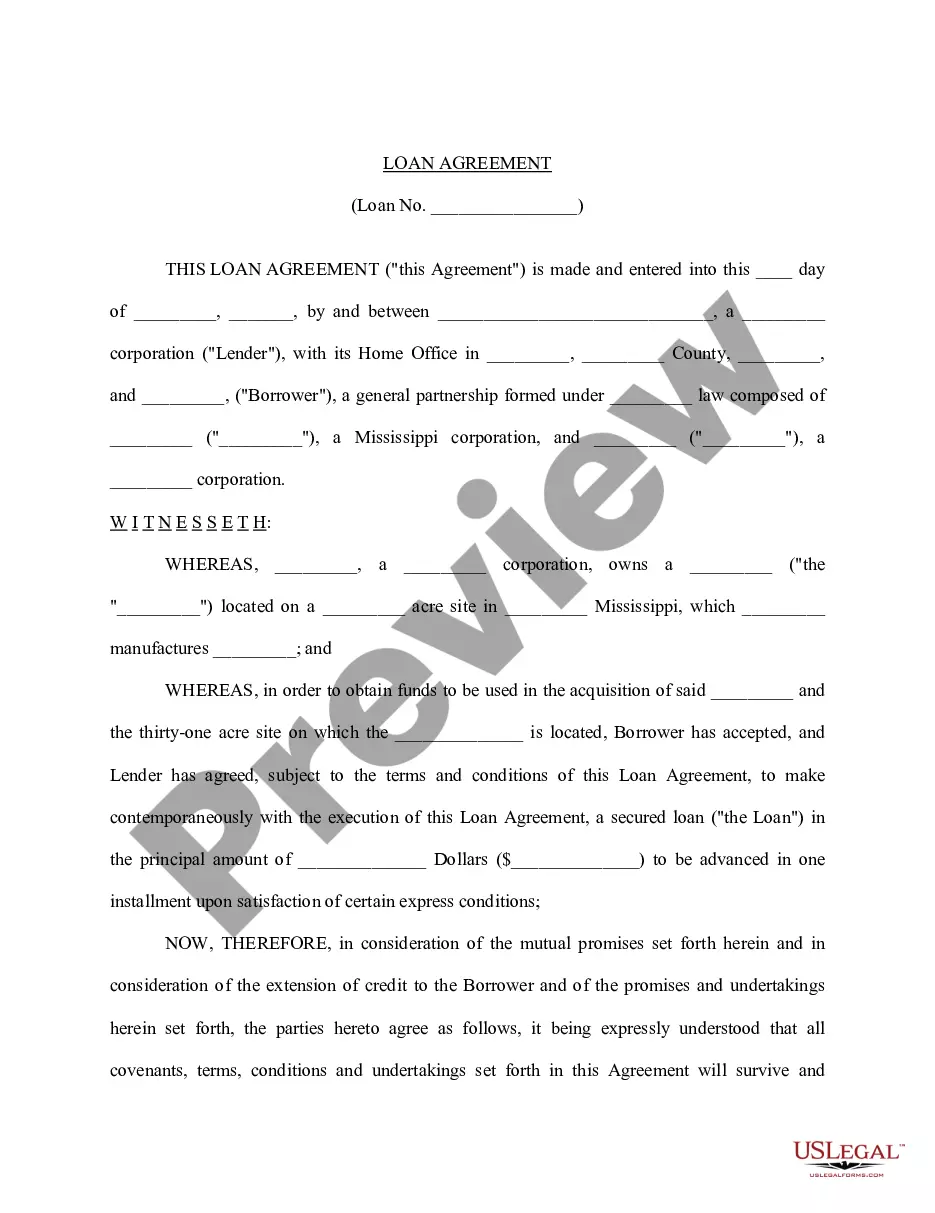

A Loan Agreement is entered into by two parties. It lists the duties, obligations and liabilities of each party when entering into the loan agreement. A Virginia Loan Agreement for Family Member is a legally binding contract that outlines the terms and conditions under which a loan is being provided by one family member to another in the state of Virginia. This agreement helps protect both parties involved and ensures that all expectations and obligations are clearly defined. The key components included in a Virginia Loan Agreement for Family Member typically include: 1. Parties Involved: Identifies the names and contact information of the lender (family member providing the loan) and the borrower (family member receiving the loan). 2. Loan Amount: States the specific amount of money being borrowed, in both numerical and written form. 3. Interest Rate: Specifies the interest rate applicable to the loan, if any. This can be a fixed or variable rate, or it may be interest-free. 4. Repayment Terms: Outlines the repayment terms, including the frequency of payments (e.g., monthly, bi-weekly), the amount of each payment, and the repayment start date. It may also include provisions for late payments or prepayment penalties. 5. Collateral: Specifies whether any collateral is required to secure the loan. Collateral can be any valuable asset, such as real estate or personal property, that serves as a guarantee that the loan will be repaid. 6. Governing Law: States that the loan agreement is subject to the laws of the state of Virginia and any disputes will be settled in a Virginia court. 7. Termination: Describes the circumstances under which the loan agreement can be terminated, such as upon full repayment or a breach of terms by either party. Different types of Virginia Loan Agreements for Family Members may include: 1. Promissory Note: A simple loan agreement that establishes the terms of a loan, including repayment details, but is not secured by collateral. 2. Secured Loan Agreement: This document outlines a loan where collateral is provided by the borrower to secure the lender's investment. If the borrower defaults on the loan, the lender can seize the collateral to recover the outstanding debt. 3. Parent-Child Loan Agreement: Specifically designed for loans between parents and children, this agreement may contain additional provisions, such as circumstances under which the loan may be forgiven or repayment terms adjusted based on the borrower's financial situation. 4. Loan Agreement with Interest: This type of loan agreement specifies an agreed-upon interest rate, ensuring that the lender receives additional compensation for the use of their money. In summary, a Virginia Loan Agreement for Family Member is a legally binding contract that protects both parties involved in a loan transaction between family members. It clearly defines the terms of the loan, repayment obligations, and helps establish a transparent and trustworthy arrangement within the family.

A Virginia Loan Agreement for Family Member is a legally binding contract that outlines the terms and conditions under which a loan is being provided by one family member to another in the state of Virginia. This agreement helps protect both parties involved and ensures that all expectations and obligations are clearly defined. The key components included in a Virginia Loan Agreement for Family Member typically include: 1. Parties Involved: Identifies the names and contact information of the lender (family member providing the loan) and the borrower (family member receiving the loan). 2. Loan Amount: States the specific amount of money being borrowed, in both numerical and written form. 3. Interest Rate: Specifies the interest rate applicable to the loan, if any. This can be a fixed or variable rate, or it may be interest-free. 4. Repayment Terms: Outlines the repayment terms, including the frequency of payments (e.g., monthly, bi-weekly), the amount of each payment, and the repayment start date. It may also include provisions for late payments or prepayment penalties. 5. Collateral: Specifies whether any collateral is required to secure the loan. Collateral can be any valuable asset, such as real estate or personal property, that serves as a guarantee that the loan will be repaid. 6. Governing Law: States that the loan agreement is subject to the laws of the state of Virginia and any disputes will be settled in a Virginia court. 7. Termination: Describes the circumstances under which the loan agreement can be terminated, such as upon full repayment or a breach of terms by either party. Different types of Virginia Loan Agreements for Family Members may include: 1. Promissory Note: A simple loan agreement that establishes the terms of a loan, including repayment details, but is not secured by collateral. 2. Secured Loan Agreement: This document outlines a loan where collateral is provided by the borrower to secure the lender's investment. If the borrower defaults on the loan, the lender can seize the collateral to recover the outstanding debt. 3. Parent-Child Loan Agreement: Specifically designed for loans between parents and children, this agreement may contain additional provisions, such as circumstances under which the loan may be forgiven or repayment terms adjusted based on the borrower's financial situation. 4. Loan Agreement with Interest: This type of loan agreement specifies an agreed-upon interest rate, ensuring that the lender receives additional compensation for the use of their money. In summary, a Virginia Loan Agreement for Family Member is a legally binding contract that protects both parties involved in a loan transaction between family members. It clearly defines the terms of the loan, repayment obligations, and helps establish a transparent and trustworthy arrangement within the family.